Resilient Compounding Through Royalty and Resource Ownership

Texas Pacific Land delivered a resilient set of results in Q3 2025, underscoring once again why the company remains one of the most distinctive and durable business models in the North American energy landscape. Even amid moderating drilling activity and a volatile commodity backdrop, the combination of vast surface acreage, perpetual mineral rights, and an expanding water-services platform continued to generate strong free cash flow and margin resilience. The quarter reaffirmed TPL’s identity not as a cyclical oil-and-gas proxy, but as a structural royalty compounder whose value compounds quietly in step with the development of the Permian Basin itself.

Revenue Performance and Core Trends

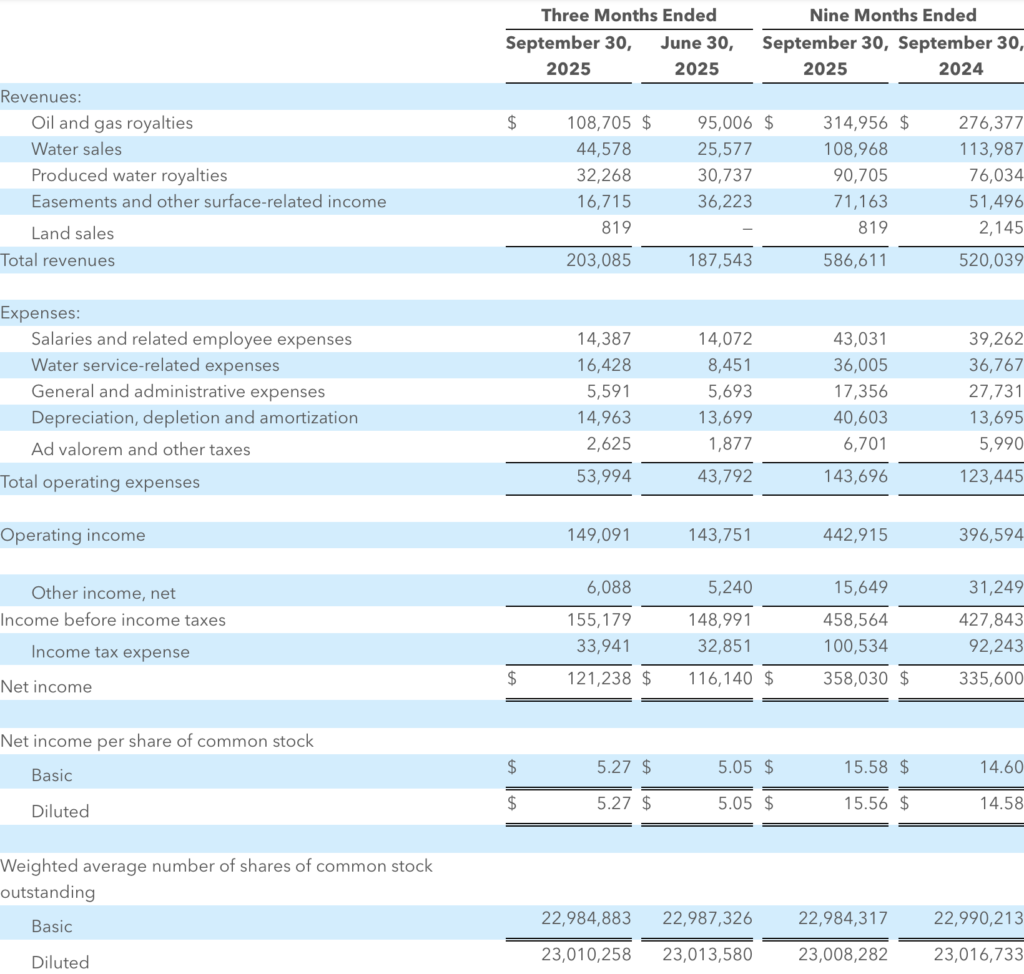

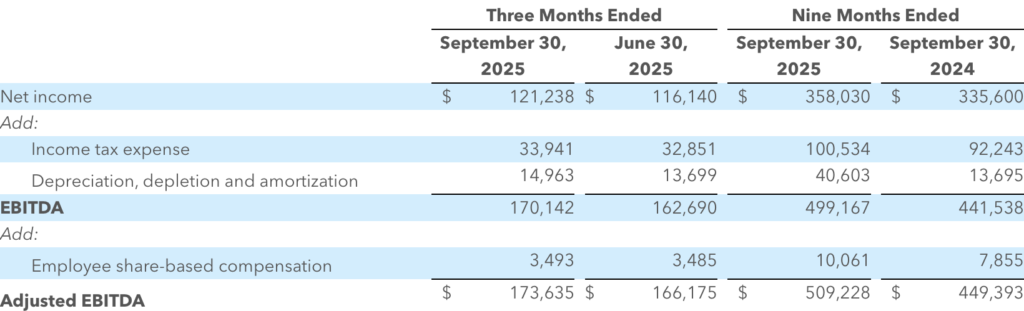

For the third quarter, total revenues rose to US $203.1 million, representing an increase of roughly 8 percent from the previous quarter. Net income reached US $121.2 million, or US $5.27 per diluted share, while adjusted EBITDA came in at US $173.6 million. These figures reflected modest sequential growth across both operating segments—land & resource management and water services—as well as disciplined cost control despite inflationary pressure in field operations.

TPL’s business remains tightly correlated with overall activity in the Permian Basin, yet the company benefits from the region’s unrivalled economics. Royalty volumes reached 36.3 thousand barrels of oil equivalent per day, up from 33.2 thousand boe/d in Q2, driven by additional well connections and a favourable production mix. The realised average price per boe improved slightly to US $34.10, supporting higher royalty revenues despite only modest changes in commodity benchmarks.

In aggregate, oil & gas royalties contributed US $108.7 million to quarterly revenue, with the balance coming from water sales, produced-water royalties, and surface income. Although surface-related income fell from the prior quarter’s elevated level—reflecting the inherently lumpy nature of easement and right-of-way payments—this was more than offset by strength in the water segment.

Royalty Segment: Quiet Compounding

TPL’s royalty and surface acreage form the core of its value proposition. The company’s land and mineral portfolio encompasses roughly 882,000 acres across West Texas, primarily within the Delaware and Midland sub-basins. These mineral interests are perpetual and unencumbered by capital obligations, meaning the company bears none of the development cost while retaining the upside from any increase in drilling density or productivity.

During the quarter, royalty revenues benefited from both higher production volumes and marginally stronger price realisations. While the company has limited ability to influence operator behaviour, the structural tailwind remains powerful: as long as the Permian continues to attract capital, TPL’s royalty stream compounds passively. The economics of this model are unmatched in their simplicity—near-100 percent margins, no depletion cost, and virtually no capital expenditure.

At quarter-end, the company reported 100.5 net producing wells on its royalty acreage, alongside 19 net wells at various stages of development. Each incremental completion directly expands the royalty base without incremental investment. This organic expansion of the royalty inventory underpins TPL’s long-term compounding thesis: production growth across the basin continuously translates into a larger, higher-yielding royalty stream.

While commodity exposure remains an unavoidable variable, management has repeatedly emphasised that the company’s model is designed to perform throughout the cycle without hedging. In practice, the absence of hedging allows TPL to capture full upside in rising markets and rely on its low cost structure to remain profitable during downturns. Q3’s results once again demonstrated the virtue of that approach.

Water Services: A Second Growth Engine

The water business continued to emerge as a second structural growth pillar. Water Services & Operations generated US $80.8 million in revenue—its highest quarterly result to date—representing nearly 40 percent of consolidated revenues. The segment includes water sales, produced-water royalties, pipeline transportation fees, and water disposal operations.

Quarterly water sales rose to US $44.6 million, compared with US $25.6 million in Q2. Produced-water royalties added another US $32.3 million, benefitting from sustained high volumes of recycled and disposed water. This momentum underscores the growing complexity and scale of Permian water logistics, an area in which TPL holds a decisive geographic advantage.

The company’s surface ownership enables it to control both water sourcing and infrastructure corridors, creating a natural monopoly over certain strategic areas. As the industry transitions toward higher levels of water recycling and reuse, TPL’s infrastructure footprint is positioned to become even more valuable. Its Orla desalination facility, currently under construction, is expected to process up to 10,000 barrels per day of produced water—further extending the company’s capabilities in treatment and reuse.

Although segment expenses increased by roughly US $8 million due to higher activity and inflationary inputs, margins remained robust, reflecting the operational leverage embedded in the business. Importantly, water services revenue tends to be more stable than royalties, offering a natural counterweight to commodity cyclicality.

Surface and Easement Income

Surface-related income, which includes easements, land sales, and other use fees, declined to US $16.7 million from US $36.2 million in the prior quarter. This volatility is typical: easement payments depend on timing of infrastructure projects such as pipelines, roads, and power lines, and can fluctuate sharply quarter to quarter. Over a longer horizon, however, these payments compound as regional development intensifies.

The underlying driver is simple—every new well pad, pipeline, or transmission corridor built across TPL land increases the monetisation opportunities for its surface estate. With tens of thousands of acres situated in core development zones, the company’s surface rights continue to represent a latent source of cash flow, even if quarterly results appear uneven.

Operating Efficiency and Financial Profile

Total operating expenses rose to US $54.0 million in Q3 from US $43.8 million in Q2, primarily reflecting higher water-service costs and one-time transaction expenses associated with recent acreage acquisitions. Despite these increases, the company maintained an EBITDA margin above 85 percent, a testament to its structurally lean operating model.

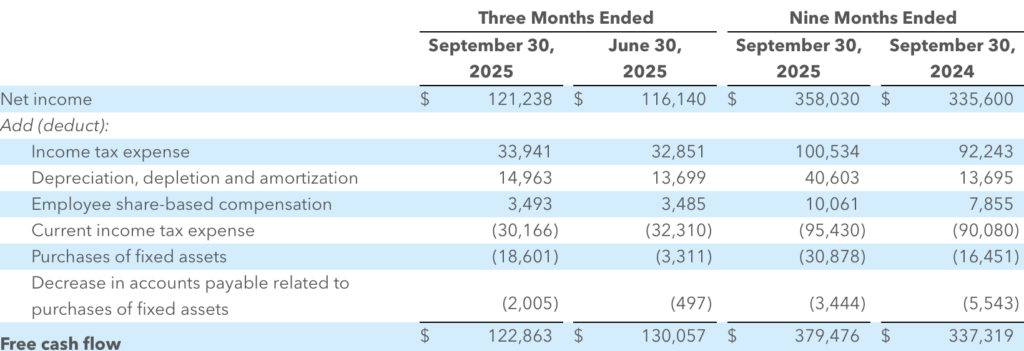

TPL generated US $122.9 million in free cash flow during the quarter, translating to a free-cash-flow margin of roughly 60 percent. This cash flow supports both shareholder returns and continued investment in land and water infrastructure. The company’s balance sheet remains pristine: even after funding significant acquisitions, debt levels are minimal and liquidity ample.

On October 23, 2025, TPL secured a new US $500 million revolving credit facility, which remains undrawn. This facility provides optionality for future growth while maintaining balance-sheet flexibility. The decision to expand liquidity without immediately drawing on it reflects management’s conservatism and preference for internal funding through cash generation.

Balance Sheet Strength and Financial Flexibility

TPL’s financial position remains exceptionally strong. The company closed the quarter with a net cash balance sheet, minimal leverage, and a newly established US $500 million revolving credit facility that provides additional liquidity. Importantly, the facility was undrawn at closing and remains undrawn today, underscoring management’s preference to maintain optional capacity rather than employ leverage for its own sake.

This facility meaningfully augments TPL’s liquidity while preserving its conservative balance-sheet posture. With both cash reserves and borrowing headroom, the company has the flexibility to act countercyclically—deploying capital into high-quality acreage or infrastructure investments during periods of market weakness, when valuations are most attractive.

Management framed this approach as part of a consistent capital philosophy: a focus on maximizing intrinsic value per share through disciplined allocation rather than opportunistic spending. In practice, that means evaluating every use of cash—whether for land acquisitions, water-infrastructure expansion, or shareholder returns—through the lens of long-term per-share compounding.

The combination of ample liquidity, net cash, and conservative financial management gives TPL a rare advantage in the resource sector: the ability to expand opportunistically when others are constrained, without sacrificing its balance-sheet strength or return discipline.

Capital Allocation and Acquisitions

One of the most noteworthy developments in the quarter was TPL’s continued expansion of its land and royalty base through targeted acquisitions. The company completed the purchase of approximately 17,306 net royalty acres (standardised to a one-eighth interest) in the Midland Basin and an additional 8,147 surface acres in Martin County, Texas. The combined transaction value was roughly US $505 million, paid entirely in cash.

These acquisitions are consistent with management’s long-term objective: consolidate high-quality acreage adjacent to its existing holdings, thereby deepening its exposure to the most prolific zones of the Permian. Management expects these newly acquired royalties to deliver double-digit pre-tax cash-flow yields even at conservative commodity assumptions (US $60 oil, US $2 natural gas).

The company also announced a three-for-one stock split in early November, a move aimed at improving liquidity and broadening shareholder participation. Although largely cosmetic, the split signals confidence in the long-term growth trajectory and desire to make shares more accessible to a wider investor base.

Importantly, capital allocation remains measured. TPL continues to pay a regular quarterly dividend—US $1.60 per share during the quarter—while retaining sufficient cash for reinvestment and opportunistic land purchases. There is little evidence of empire-building or over-leveraging; the company’s preference for organic compounding through acreage expansion and water infrastructure build-out remains intact.

Governance and Corporate Structure

While operational execution has been strong, corporate governance continues to be a topic of investor focus. TPL’s complex historical evolution—from a land trust formed out of a nineteenth-century railroad bankruptcy to a modern C-Corporation—has created lingering disputes over oversight and shareholder rights.

Management’s tone in recent quarters suggests a greater willingness to engage constructively with shareholders, and the formal separation of the Board Chair and CEO roles earlier in the year marked progress. Nonetheless, transparency around related-party arrangements and capital-allocation criteria remains an area where the company could further strengthen investor confidence.

That said, TPL’s governance trajectory is improving, and the business economics remain strong enough to withstand temporary perception headwinds. For most long-term investors, governance risk is secondary to the unparalleled asset quality and free-cash-flow generation that the company consistently demonstrates.

Strategic Positioning within the Permian Basin

TPL’s competitive advantage is geographic permanence. Its surface and mineral rights sit across some of the most active drilling corridors in the United States, ensuring that every incremental investment by operators—from majors like Exxon Mobil and Chevron to independent producers—indirectly enhances TPL’s cash flow.

The Permian remains the centrepiece of U.S. hydrocarbon supply growth, and while production growth is moderating, the basin’s long-term outlook remains positive. Decline rates are lower, productivity per well remains high, and consolidation among operators has improved capital discipline. This environment benefits TPL: fewer, larger, better-capitalised operators tend to focus development on core acreage where TPL’s interests are concentrated.

Additionally, infrastructure build-out across West Texas continues unabated. New gathering systems, power transmission lines, and water-recycling facilities all require access rights, driving a steady flow of easement income. The same activity supports the water business, as producers seek reliable, cost-effective solutions for sourcing and disposing of water volumes that can exceed several barrels per barrel of oil produced.

In this ecosystem, TPL functions as a silent toll collector—earning recurring royalties, leasing rights-of-way, and selling or treating water—all without assuming drilling or commodity risk. The company’s economic exposure is asymmetric: upside participation in development, downside protection through low fixed costs.

Operating Leverage and Margin Resilience

The quarter’s margin performance highlights the inherent operating leverage in TPL’s model. Incremental revenue growth flows disproportionately to the bottom line, since fixed costs remain minimal. As the royalty and water bases expand, unit economics improve further.

This leverage works in both directions; a sharp decline in commodity prices or drilling could compress margins temporarily. However, the combination of royalty, surface, and water revenues provides a natural buffer. The correlation between oil prices and total revenue is meaningful but not absolute. For instance, even in periods of weaker commodity pricing, infrastructure and water activity can remain elevated due to ongoing production maintenance.

Over time, we expect TPL’s blended margin profile to stabilise in the high-70s to low-80s percent range at the EBITDA level—an extraordinary figure for an asset-based enterprise. Few businesses in the public markets can sustain comparable levels of profitability with such limited capital intensity.

Risks and Considerations

Despite its strengths, TPL is not immune to risk. The most immediate is commodity-price exposure: while royalty volumes may grow, realised revenue per boe will still fluctuate with oil and gas prices. The company’s decision not to hedge remains a double-edged sword—enhancing long-term returns but exposing near-term results to volatility.

Operationally, surface and easement income will likely continue to exhibit quarter-to-quarter swings. Investors should interpret these fluctuations as timing differences rather than structural weakness. Over a multi-year horizon, aggregate surface income has trended higher in tandem with the region’s infrastructure expansion.

A more subtle risk lies in the evolving regulatory and environmental landscape surrounding water usage in West Texas. Increasing scrutiny of produced-water disposal and seismicity could raise compliance costs or limit certain operations. TPL’s investment in desalination and reuse capabilities is a proactive step toward mitigating this risk and aligning the business with the industry’s shift toward sustainable water management.

Finally, governance remains an ongoing watch-item. While improvements are visible, maintaining robust oversight will be crucial as the company grows larger and more complex.

Long-Term Outlook

TPL’s long-term thesis remains remarkably straightforward: own irreplaceable real assets in the most productive oil basin in North America, participate in its development through high-margin royalties and services, and compound free cash flow with minimal reinvestment needs. Each incremental well drilled on its acreage expands the royalty base; each new infrastructure project enhances the monetisation of its surface estate.

The company’s expansion into water infrastructure adds a second, complementary growth vector that is less cyclical and more volume-driven. Together, these businesses form a self-reinforcing ecosystem: water operations make the land more valuable, while land ownership provides exclusive access to water opportunities.

Yet the structural potential of TPL’s land portfolio extends far beyond hydrocarbons and water. The combination of abundant surface acreage, existing transmission easements, and access to low-cost power positions the company to benefit from the next wave of industrial development in West Texas: data centers, renewable integration, and digital infrastructure.

As generative AI workloads and high-density cloud computing create unprecedented demand for power-hungry data facilities, the Permian Basin’s energy infrastructure and available land are gaining attention as a cost-effective alternative to traditional data-center hubs. TPL’s holdings, many of which are adjacent to transmission lines and existing substations, offer ideal conditions for such development.

The company’s land can serve both as a direct host for data center projects and as a strategic counterparty in long-term land or power-usage agreements, providing stable, recurring surface income not tied to the commodity cycle. In parallel, renewable developers continue to explore hybrid solar-and-wind installations across West Texas to serve precisely this type of load. TPL’s position as a neutral, capital-light landowner gives it the ability to monetise this convergence of energy and computing without deploying significant capital itself.

Management has not yet formalised a large-scale data-center partnership, but discussions across the industry suggest increasing interest from hyperscale operators seeking energy-secure, affordable land parcels in the region. Should even a handful of these opportunities materialise over the next decade, the incremental surface income could meaningfully diversify TPL’s revenue mix and further decouple its long-term value from the commodity cycle.

With a fortress balance sheet, high returns on invested capital, and structural exposure to one of the world’s most enduring energy basins, TPL continues to stand apart from both traditional E&P companies and real-estate owners. It occupies a rare niche—a perpetual royalty compounding machine whose intrinsic value grows quietly with every passing quarter of basin development, now with potential optionality in the digital infrastructure economy that is beginning to take shape across the American Southwest.

Conclusion

Q3 2025 reaffirmed Texas Pacific Land’s position as one of the most efficient and durable compounding vehicles in the public markets. The quarter’s modest revenue growth, strong free-cash-flow generation, and continued expansion of the water segment highlight the strength of the company’s dual-engine model.

Short-term noise—whether from commodity prices, governance debates, or quarterly surface-income swings—does little to alter the underlying trajectory. The company’s assets are finite, irreplaceable, and directly leveraged to the gradual industrialisation of the Permian Basin. Every mile of new pipeline, every well completed, and every barrel of water moved across its acreage adds to TPL’s long-term earning power.

In our view, Texas Pacific Land remains a uniquely positioned royalty compounder: asset-light, margin-rich, and endowed with structural tailwinds that few businesses can replicate. Its performance in Q3 2025 once again demonstrated that, while the Permian may experience cycles, the compounding of TPL’s intrinsic value is a steady and enduring process.