Building the Surface Economy of the Permian Basin

LandBridge Company LLC delivered another strong quarter in Q3 2025, underscoring the strength of its surface- and water-focused business model. As industrial activity in the Permian Basin expands beyond drilling into water logistics, infrastructure, and renewable development, LandBridge continues to establish itself as one of the most strategically positioned land platforms in the region.

Unlike traditional royalty companies, LandBridge has always maintained minimal exposure to oil and gas prices, deriving the majority of its revenue from surface use, water operations, and infrastructure leasing. This structure provides remarkable resilience: cash flows are recurring, capital-light, and largely insulated from commodity volatility.

Q3 reaffirmed this model, highlighting steady growth, strong margins, and rising optionality for future development across digital and renewable infrastructure.

Business Model and Strategic Context

LandBridge’s foundation is its ownership and management of over 300,000 surface acres across Loving, Reeves, Winkler, and Ward counties—one of the most active industrial corridors in the Permian Basin. The company’s business model revolves around monetising these surface and subsurface rights through water handling, easements, land leases, and infrastructure access, rather than through direct oil and gas production.

This approach offers two defining advantages:

- Capital efficiency – With minimal operating expenditure and no drilling costs, margins remain among the highest in the energy-adjacent real-asset universe.

- Cash-flow stability – Because income is driven by recurring surface and infrastructure activity rather than commodity prices, earnings volatility is low and visibility high.

In essence, LandBridge operates as a real-asset toll collector on the industrialisation of the Permian Basin. Each new pipeline, power line, road, or facility that crosses its acreage enhances long-term value while requiring almost no incremental capital investment.

Q3 2025 Performance Review

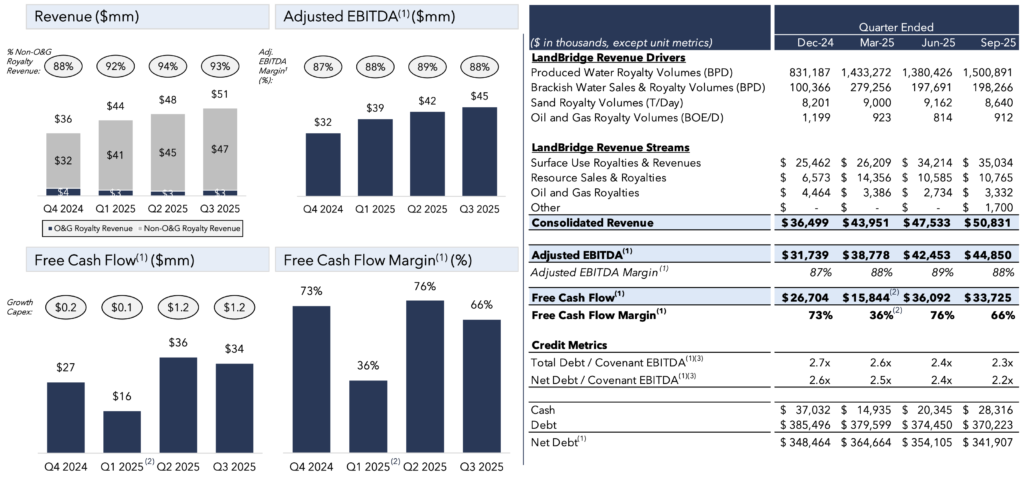

LandBridge reported revenue of US $50.8 million, an increase of roughly 78 % year-over-year and 7 % quarter-over-quarter, marking the sixth consecutive quarter of top-line and EBITDA growth.

- Net income: US $20.3 million, representing a 40 % net margin.

- Adjusted EBITDA: US $44.9 million (up 79 % YoY), with an 88 % margin.

- Operating cash flow: US $34.9 million; free cash flow: US $33.7 million, reflecting a 66 % conversion ratio.

These results highlight the durability of LandBridge’s capital-light model and its ability to generate strong returns even in a mixed commodity environment. None related party revenues continue to outpace related party revenues

Segment Performance and Growth Drivers

Water and Resource Sales

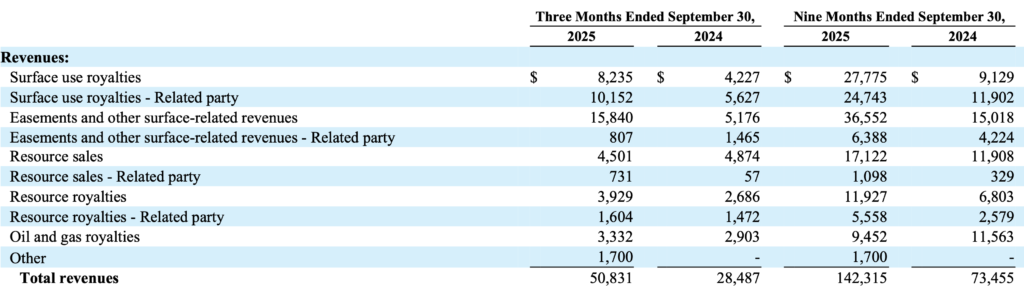

Water remains the backbone of LandBridge’s operations. Q3 resource-sales and royalty revenue reached US $10.8 million, driven by higher produced-water volumes and new water-handling contracts. The company’s 37,500-acre acquisition in the Stateline area expanded its control over critical pore space and disposal corridors—assets expected to become increasingly valuable as water recycling and injection capacity tighten in the Permian.

Because water management is a perpetual requirement of regional production and infrastructure maintenance, this segment provides LandBridge with recurring, non-cyclical cash flow that compounds alongside broader basin activity.

Surface Use and Infrastructure Leasing

Surface-use revenues—easements, right-of-way payments, industrial leases, and renewable-site transactions—remain LandBridge’s largest contributor. The company’s role is straightforward: provide access to strategically located land and receive recurring payments as industrial operators, utilities, and midstream companies expand their footprint.

During Q3, LandBridge closed a long-term lease with a subsidiary of ONEOK for a gas-processing facility in Loving County and finalised the sale of a 3,000-acre solar-generation site in Reeves County to a major infrastructure developer. These transactions demonstrate the ongoing monetisation potential of LandBridge’s surface estate.

Oil and Gas Royalties

Oil and gas royalties accounted for just over US $3 million of quarterly revenue—less than 7 % of total income. This limited exposure has been a consistent feature of LandBridge’s structure since inception, not a recent pivot. The company benefits indirectly from drilling activity through surface fees and water demand but is not meaningfully dependent on commodity prices.

This inherent diversification distinguishes LandBridge from traditional royalty peers: it participates in regional growth while remaining insulated from oil and gas price swings.

Capital Allocation and Financial Strength

LandBridge’s high margins translate directly into free cash flow. The company generated US $33.7 million in FCF during the quarter while spending only US $1.2 million in capex, underscoring the minimal reinvestment required to sustain operations.

Financing outflows totalled US $25.8 million, comprising US $14.8 million in dividends, US $5 million in debt repayments, and US $5.7 million in tax withholdings tied to share-based compensation. A quarterly dividend of US $0.10 per share was declared, signalling the continuation of a balanced capital-return program.

The balance sheet remains robust, with low leverage and substantial liquidity—providing flexibility to pursue opportunistic acreage acquisitions and infrastructure partnerships.

Management’s capital philosophy emphasises intrinsic-value compounding over absolute expansion, a hallmark of long-term discipline.

Strategic Positioning and Outlook

LandBridge’s outlook is defined by the enduring strength of its water and surface-use franchise and by the emerging potential to host digital and renewable infrastructure on its land. The company’s strategy has always centred on monetising its extensive surface estate across multiple industrial channels—not merely hydrocarbons.

1. Water and Surface-Use Leadership (updated)

Water remains the backbone of LandBridge’s model, and Q3 commentary added important detail to the medium-term growth path. Resource sales and royalties reached US $10.8 million in the quarter, supported by higher produced-water volumes and new handling agreements. The recently closed ~37,500-acre acquisition (the “1918” package across Loving and Reeves) is immediately cash-flowing and expected to contribute ~US $20 million of EBITDA in 2026 on a conservative, no-growth underwriting base. Beyond the near-term contribution, management highlighted line of sight to materially higher earnings over a 3–4 year horizon as pore-space is commercialized and as the footprint opens new corridors for water logistics and surface activity.

Two elements are particularly notable. First, the eastern / Southern Loving County position adds ~900,000 bpd of incremental pore-space capacity, deepening inventory and extending LandBridge’s reach into areas that unlock additional commercial opportunities. Management noted that at prevailing market royalty rates, this pore-space alone could support “mid-$50 millions” of EBITDA once ramped, with timing driven by the pace of operator contracting and permitting. Second, the western portion of the package sits amid a dense build-out of transmission and power infrastructure, making it well suited for clean-energy and digital-industrial projects that rely on power adjacency and access.

Surface-use revenues continue to reflect this optionality. During Q3, LandBridge finalized the sale of a ~3,000-acre solar site in Reeves County (proposed capacity ~250 MW) with an upfront payment, contingent milestone payments over the development cycle, and recurring revenue once operational. The company also executed a long-term lease with a subsidiary of ONEOK for a natural-gas processing facility in Loving County—structured as upfront consideration plus annual payments, with additional recurring income from associated infrastructure (pipelines, electrical interconnects, and access corridors) as the build-out proceeds.

Taken together, these developments reinforce a core theme of the LandBridge thesis: contiguous surface control + pore-space stewardship + infrastructure adjacency yields recurring, capital-light cash flows that compound as West Texas industrializes.

2. Power Infrastructure and Data-Center Initiatives (updated)

Management’s Q3 remarks indicate that power and data-center opportunities are moving from concept toward active commercialization. Executives described “accelerating” progress with multiple blue-chip counterparties, noting that discussions have evolved into packaged negotiations that pair site control with power partnerships and water availability, in locations that also benefit from favorable fiber proximity. In other words, LandBridge is not simply a landlord—it is increasingly positioned as an integrated land–power–water solution provider for large, energy-dense digital infrastructure.

While no definitive data-center agreements have been announced, management emphasized that the economic fundamentals of West Texas made this wave “inevitable”—and that LandBridge is further along in conversations than many appreciate. The company expects to share milestones as they are finalized, acknowledging commercial sensitivities and confidentiality constraints in the interim. Parallel power-infrastructure initiatives are also advancing to improve the attractiveness of key sites for clean-energy generation and compute loads, recognizing that power adjacencyis the gating factor in hyperscale deployment.

The strategic message is clear: as hyperscalers and power providers increasingly pursue coordinated, bundled solutions, LandBridge’s ability to deliver de-risked, shovel-ready sites with surface, pore-space, water, and transmission accesscreates a competitive moat that is hard to replicate.

3. Pore-Space Scarcity as a Structural Advantage (new)

Q3 disclosures sharpened the secular tailwind behind produced-water royalties. Management presented analysis indicating that, due to over-concentration and geological over-pressure along parts of the state line, existing produced-water infrastructure in the Delaware Basin is expected to lose operating capacity over time, even as regional produced-water volumes rise through 2035. The result, on current trajectories, could be a ~9 million barrels/day shortfall in disposal capacity by year-end 2035—a gap that will require new pore-space access and new handling corridors.

Crucially, pore-space is not a commodity. LandBridge’s highly contiguous, geologically resilient acreage—intentionally stewarded to avoid over-concentration—represents premium disposal inventory in the most constrained sub-basins. This drives two advantages: (i) durability and pricing power in produced-water royalties as operators secure long-term access; and (ii) commercial velocity, as counterparties increasingly transact directly with LandBridge to lock in rights. The company’s minimum-volume commitment and pore-space access agreement with a major operatorlast quarter exemplifies this shift toward direct, multiyear arrangements that prioritize pore-space quality and control.

4. Consistently Low Commodity Exposure

LandBridge’s limited reliance on oil and gas royalties has long protected its earnings from price volatility. Most of its revenues are tied to fixed or volume-based surface contracts, water royalties, and infrastructure fees that do not fluctuate materially with commodity benchmarks.

This structure results in a more predictable, infrastructure-like earnings profile that should continue to attract investors seeking stability within the broader energy-transition landscape.

5. The Broader Vision

LandBridge is effectively constructing the surface economy of the Permian Basin—a network of rights, easements, and infrastructure corridors that enable every facet of industrial expansion, from hydrocarbons to renewables to data-driven industries.

The company’s strategy is less about transition and more about continuity of opportunity: the same land that once enabled drilling now underpins water, power, and digital infrastructure. LandBridge’s goal is to monetise this convergence without assuming operational or commodity risk, creating a durable and scalable real-asset platform.

Risks and Considerations

The principal risks to the thesis remain operational and timing related. Drilling slowdowns can temporarily reduce surface-use intensity; infrastructure and renewable projects often depend on lengthy permitting and development cycles; and competitive pressures could raise acquisition costs for prime acreage.

Nevertheless, LandBridge’s diversified revenue mix, capital efficiency, and strong balance sheet offer substantial protection. The company can remain patient, monetising opportunities selectively while maintaining high free-cash-flow margins.

Conclusion

LandBridge’s Q3 2025 results reinforce its identity as a high-margin, surface- and water-driven land platformoperating in the heart of the Permian Basin. With 88 % EBITDA margins, robust free cash flow, and growing opportunities in renewable and digital infrastructure, the company continues to demonstrate that energy-linked real assets can provide both growth and stability.

The power and data-center pipeline is now visibly advancing: management reports active, multi-party negotiationswith blue-chip counterparties and an industry shift toward bundled land-plus-power solutions that dovetail with LandBridge’s core competencies. At the same time, the 1918 acquisition adds near-term EBITDA (conservatively ~US $20 million in 2026) and unlocks 3–4 years of pore-space and surface monetization, including “mid-$50 millions” of potential EBITDA from pore-space at prevailing rates once contracted and ramped. Layer in renewables (e.g., the ~3,000-acre, ~250 MW solar transaction with milestones and recurring revenue) and industrial leasing (e.g., the ONEOK gas-processing facility with upfront and recurring infrastructure payments), and we see multiple, parallel growth engines compounding with limited capital intensity.

The accelerating alignment between energy, power, and compute suggests that LandBridge’s acreage could become a foundational hub for West Texas’s next industrial chapter—where produced water, transmission corridors, and data processing capacity converge within a single, surface-led platform. We expect the company to prioritize disclosure as milestones are finalized, but even absent signed data-center agreements today, the commercial trajectory and asset positioning now appear decisively favorable.

For investors seeking exposure to the region’s long-term industrial build-out—without the volatility of oil and gas prices—LandBridge stands as a unique vehicle: capital-light, cash-rich, and positioned at the confluence of water, infrastructure, and the digital frontier.