Introduction & Investment Overview

Miami International Holdings, Inc. (MIAX) serves as the holding company for a diversified portfolio of securities exchanges and clearing facilities. Established initially as a private challenger in the U.S. options market, the company has evolved into the fourth major pillar of the American exchange infrastructure, operating alongside legacy incumbents Cboe Global Markets, Nasdaq, and Intercontinental Exchange (NYSE).

Following its initial public offering in August 2025, MIAX has transitioned from a niche technology operator into a fully integrated financial utility. The company’s ecosystem now encompasses four distinct U.S. options exchanges—MIAX Options, MIAX Pearl, MIAX Emerald, and the recently launched MIAX Sapphire—collectively capturing approximately 18% of total U.S. multi-listed options volume. Beyond its core options franchise, the company has aggressively pursued vertical integration through the acquisition of the Minneapolis Grain Exchange (MGEX), granting it a coveted Derivatives Clearing Organization (DCO) license, and expanded internationally via the Bermuda Stock Exchange (BSX) and The International Stock Exchange (TISE).

This analysis seeks to evaluate MIAX’s standing in the post-IPO landscape. It examines the structural tension currently visible in the company’s financial profile: a dichotomy between rapid top-line revenue expansion and the optical GAAP losses associated with its capitalization events. Furthermore, this report investigates the „utility-like“ characteristics of the business—specifically its proprietary technology stack and clearing capabilities—to determine whether the market’s current valuation framework appropriately accounts for the company’s long-term competitive moat and scalability.

I. Executive Summary: The Asymmetric Disrupter

MIAX represents a classic „challenger“ play in the global exchange oligopoly. While the legacy incumbents (Cboe, Nasdaq, NYSE/ICE) trade at mature multiples with low-single-digit organic growth, MIAX is in a hyper-growth phase (+57% YoY revenue growth in Q3 2025) masked by optically ugly GAAP losses driven by one-time IPO-related expenses.

The Core Thesis: The market is currently pricing MIAX as a commoditized exchange operator, ignoring its superior technology stack (latency advantage) and the margin expansion inherent in its recent vertical integration (clearing/futures). We believe MIAX is mispriced relative to its growth trajectory and presents a 30-40% upside as GAAP profitability normalizes in 2H 2026.

II. The Horizon Kinetics Thesis: A Blue-Chip in Disguise

To understand the durability of the MIAX thesis, we must look at the asset class through the lens of long-term capital accumulators. Horizon Kinetics (HK), an early strategic backer, has correctly identified the „category error“ the market is making with MIAX.

As HK articulated in their recent commentary:

„MIAX, like most IPOs, has yet to achieve normalized scale economies. But unlike most IPOs, it is of a blue-chip character with near-perpetual expected longevity. Securities exchanges—a critical mechanism for capital formation and liquidity—are the very oldest continually operated publicly traded companies in the world; they don’t fail, dwindle away or get displaced.“

This is the crux of the defensive argument. Exchanges are natural monopolies or oligopolies protected by immense regulatory moats. Once liquidity establishes a „gravity well“ at an exchange, it is nearly impossible to displace.

HK further illuminates the hidden value of the Minneapolis Grain Exchange (MGEX) acquisition, which acts as the cornerstone of MIAX’s futures ambition:

„MGEX owned a highly valuable but underutilized asset: one of the handful of registered derivatives clearing licenses in the U.S… MIAX’s advantage was superb technology, but it lacked a clearing license, which hobbled its effectiveness. MGEX had a coveted clearing license, which could be deployed to great advantage across the multiplicity of futures products that MIAX envisioned.“

The valuation disconnect between private and public valuation of these assets is staggering. HK highlighted that in 2009, one could theoretically acquire the entire MGEX exchange (seats, real estate, cash, and clearing license) for roughly $31 million. Today, that license alone underpins a multi-billion dollar futures strategy for MIAX. Public markets pay a massive premium for liquidity and „packaged“ revenue streams, and MIAX is the vehicle capitalizing on this arbitrage.

III. Business Analysis & Market Structure

MIAX is fundamentally miscategorized by the general market. It is not merely a venue for exchanging securities; it is a technology company monetizing the „latency arms race.“ While legacy incumbents rely on entrenched liquidity pools, MIAX has weaponized market microstructure to systematically dismantle the oligopoly of Cboe, Nasdaq, and NYSE.

The company operates a vertically integrated „kill chain“ that captures order flow at every stage of the trade lifecycle—from execution (Exchanges) to clearing (MIAX Futures/MGEX) to listing (TISE/BSX).

1. The Options Fortress (The Cash Cow)

Options trading is the engine room of the MIAX thesis, generating the bulk of free cash flow. Unlike competitors that often force a „one-size-fits-all“ model, MIAX has built a diversified portfolio of four distinct exchanges. This multi-platform strategy allows them to capture 100% of the addressable market by tailoring the „rules of engagement“ to specific trader types.

- MIAX Options (The Institutional Heavyweight):

- Model: Traditional „Pro-Rata“ allocation.

- Target Client: Market Makers (MMs) and Institutional Banks.

- Microstructure Physics: In a Pro-Rata model, fill priority is determined by size, not just price or speed. This encourages „whales“ like Citadel, Susquehanna, and Wolverine to post massive liquidity (e.g., 5,000 contracts on the bid) because they know they will be rewarded with a larger percentage of the trade. This venue is the bedrock of MIAX’s liquidity stability.

- MIAX Pearl (The Speed Demon):

- Model: „Price-Time“ priority with Maker-Taker pricing.

- Target Client: High-Frequency Trading (HFT) firms and Algorithmic Liquidity Removers.

- Microstructure Physics: Here, speed is king. The first firm to the price gets the fill. MIAX Pearl pays the highest rebates in the industry (up to ~$0.52 per contract) to liquidity providers („Makers“). This effectively subsidizes the spreads, creating a hyper-efficient market that attracts algo-routers seeking the lowest net cost execution.

- MIAX Emerald (The Hybrid):

- Model: A complex hybrid of Pro-Rata and Maker-Taker.

- Strategic Value: Emerald captures the „overflow“ and complex order types (e.g., multi-leg spreads) that don’t fit cleanly into the binary world of Pearl or Standard Options. It minimizes „leakage“ of complex institutional flow to Cboe’s C2 exchange.

- MIAX Sapphire (The Retail Capture Engine — Launched Aug 2024):

- Model: Taker-Maker (also known as „Inverted“ pricing).

- Target Client: Retail Wholesale Brokers (e.g., Robinhood, Schwab flow routed via Citadel/Virtu).

- Microstructure Physics: This is MIAX’s most aggressive strategic move. In this model, the exchange pays a rebate to the Taker (the retail order) and charges the Maker. This structure is mathematically designed to attract retail flow, which is considered „toxic-free“ (uninformed) and highly desirable for Market Makers.

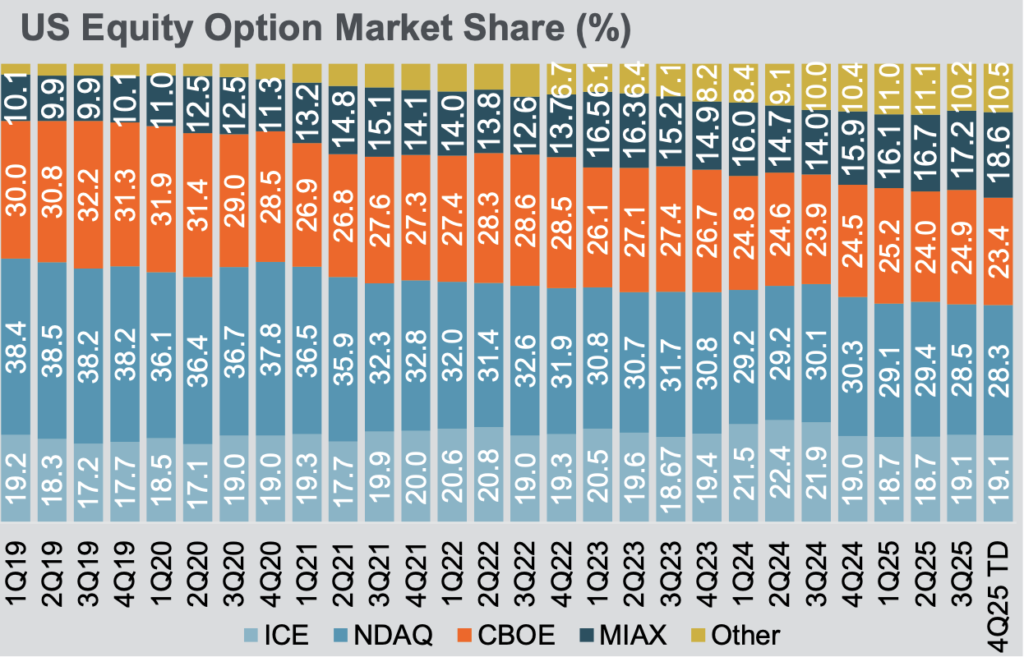

- Performance: Since its electronic launch in August 2024 and physical floor opening in September 2025, Sapphire has been a rocket ship. By Q4 2025, it helped drive the total MIAX Exchange Group market share to a record 18.2%, proving that MIAX can successfully siphon retail flow away from Nasdaq PHLX.

By operating all four market models, MIAX has effectively „internalized“ the competition. In the past, if a broker-dealer changed their routing logic to favor rebates over fill quality, that flow would leave the exchange. Now, if a broker shifts from „Pro-Rata“ to „Maker-Taker,“ the flow simply moves from MIAX Options to MIAX Pearl. The revenue stays in the house. This reduces the „churn risk“ that typically plagues challenger exchanges.

2. Vertical Integration & The „Blue-Chip“ Moat

The true long-term value of MIAX lies in its transition from a „rent-taker“ (exchange) to a „rule-maker“ (clearing house).

- The Futures Alpha (MGEX & Onyx):

- As Horizon Kinetics astutely observed, the acquisition of the Minneapolis Grain Exchange (MGEX) was a masterstroke of regulatory arbitrage. MIAX did not buy MGEX for its wheat contracts; they bought it for the Derivatives Clearing Organization (DCO) license.

- Why this matters: In the US, obtaining a new clearing license is a multi-year, multi-million dollar regulatory purgatory. By acquiring MGEX (a solvent, 100+ year-old entity), MIAX leapfrogged the line.

- MIAX Futures Onyx: Leveraging this license, MIAX launched the Onyx platform in 2025. This platform hosts proprietary products like the SPIKES Volatility Index, a direct competitor to Cboe’s VIX. While VIX is the „Goliath“ with massive volume, SPIKES uses SPY ETF data (rather than SPX index data) to offer a cheaper, more accessible volatility hedge. Because MIAX owns the clearing house (MGEX), they keep 100% of the economics on every SPIKES trade, compared to the ~40% margin they make on multi-listed options.

- 2025 Performance: MIAX Futures reached an annual ADV record of nearly 13,000 contracts in 2025. While small compared to options, this is high-margin, proprietary volume that cannot be traded anywhere else.

- Equities (The Growth Vector):

- MIAX Pearl Equities: Utilizing the same low-latency „binary“ technology stack as the options exchange, Pearl Equities has established a foothold in the cash equities market. While market share has stabilized around 1.0% (facing fierce competition from off-exchange dark pools), it serves as a critical „bundle“ for broker-dealers who want a single connection point for both asset classes.

- International Strategy (The Listings Play):

- The International Stock Exchange (TISE) & Bermuda (BSX): These acquisitions are not vanity projects; they are listing engines.

- The Play: TISE (based in Guernsey) and BSX (Bermuda) are premier venues for listing international debt securities and Insurance-Linked Securities (ILS). They offer issuers a „recognized exchange“ status for tax purposes without the burdensome Sarbanes-Oxley requirements of a full NYSE listing.

- Scale: TISE alone lists over 4,000 securities with a total market value exceeding £750 billion. This provides a steady, recurring „annual listing fee“ revenue stream that is completely uncorrelated to trading volumes or market volatility.

3. Strategic Catalysts: The B500 & The Robinhood Deal

Two specific developments in late 2025 and early 2026 have fundamentally de-risked the growth thesis:

- The „S&P Killer“ (Bloomberg 500 Futures): For decades, the S&P 500 ecosystem has been the monopoly of S&P Global and CME. MIAX has partnered with Bloomberg Index Services to launch futures on the Bloomberg 500 Index (B500), going live on the Onyx platform on February 23, 2026. The B500 tracks the same large-cap US equity universe as the S&P 500 but without the exorbitant licensing fees. Because MIAX owns the clearing house (MGEX), they can undercut CME’s fees while retaining higher margins. This product does not need to destroy the S&P 500 franchise to be successful; capturing just 2-3% of the SPX/ES volume would add estimated $50M-$80M in high-margin annual revenue.

- The Robinhood & Susquehanna Joint Venture: In November 2025, MIAX announced the sale of a 90% equity stake in its subsidiary, MIAXdx (formerly LedgerX), to a consortium led by Robinhood Markets (HOOD) and Susquehanna International Group (SIG). While MIAX retains a strategic minority interest, the true value of this deal is the alignment. By partnering with Susquehanna—one of the world’s largest option market makers—MIAX solidifies its relationship with the firm that controls a massive percentage of retail order flow. This virtually guarantees that SIG will continue to prioritize routing flow to MIAX Sapphire and MIAX Pearl. Furthermore, Robinhood’s entry into the „Event Contract“ (Prediction Market) space via this license acts as a „Trojan Horse,“ potentially driving millions of retail users into an ecosystem where MIAX holds a royalty interest.

4. The Technology Advantage: The „Latency Arms Race“

MIAX’s core IP is its proprietary trading engine, built on a highly deterministic „binary“ architecture.

- The Problem: In modern markets, „average latency“ is irrelevant; „tail latency“ (outliers) is what kills trading firms. If an exchange is fast 99% of the time but „hangs“ for 5 milliseconds during a market crash, market makers get run over.

- The MIAX Solution: MIAX’s system offers wire-order determinism. This means the processing time for an order is consistent to the nanosecond, regardless of market load.

- Commercial Impact: This technological superiority allows Market Makers to quote tighter spreads on MIAX exchanges with less risk. Tighter spreads organically attract more order flow, creating a virtuous cycle that competitors with legacy tech stacks (like Cboe’s older infrastructure) struggle to replicate without a total platform rewrite.

| Feature | MIAX Strategy | Competitor Vulnerability |

| Market Structure | Owns ALL 4 models (Pro-Rata, Maker-Taker, Hybrid, Taker-Maker). | Competitors often fragmented; Cboe relies heavily on exclusivity. |

| Clearing | Vertical Integration via MGEX (Owns the Clearing House). | Most challenger exchanges rely on third-party clearing (margin leakage). |

| Technology | Newest stack (2012+), deterministic latency. | Legacy exchanges burdened by 20+ year old „spaghetti code.“ |

| Growth Profile | +57% Revenue Growth (Q3 ’25). | Incumbents growing at GDP-like rates (4-6%). |

IV. Financial Analysis: The „J-Curve“ Inflection

The market’s current pricing of MIAX reflects a superficial reading of the GAAP P&L statement. A granular decomposition of the Q3 2025 results reveals a company exiting the „cash burn“ phase of its lifecycle and entering the „operating leverage“ phase (the steep upward slope of the J-Curve).

1. Hyper-Growth in a Mature Sector The exchange industry is typically characterized by GDP-plus growth (4-6%). MIAX is an outlier, delivering „venture-style“ growth at scale.

- Revenue Velocity: MIAX reported $109.5 million in Net Revenue for Q3 2025, a massive 57% increase YoY. This was not a low-base effect; it was driven by organic volume gains and the successful integration of the Sapphire exchange.

- The Sapphire Effect: The launch of MIAX Sapphire (August 2024) and its physical trading floor (September 2025) acted as a step-function catalyst. By Q4 2025, this new venue helped push the total MIAX Exchange Group market share to a record 18.2%, up from ~14% the prior year.

- Proprietary Alpha: While options volume fluctuates with the market, MIAX Futures (proprietary products) reached a record Annual ADV of nearly 13,000 contracts in 2025. This revenue is „sticky“ and carries significantly higher margins than multi-listed options because MIAX owns the clearing.

2. The Margin Expansion Story (The „60-Cent Dollar“) The most critical metric in this thesis is the „incremental margin“—how much of every new dollar of revenue falls to the bottom line. Exchanges have high fixed costs (technology servers, regulatory compliance) but near-zero variable costs.

- Adj. EBITDA Explosion: Q3 Adjusted EBITDA surged 157% YoY to $48.0 million.

- Margin Velocity: EBITDA margins expanded by a staggering 1,690 basis points, jumping from 26.9% to 43.8%.

- Interpretation: The business has passed its break-even threshold. Every incremental $10 million in revenue is now generating ~$6.0 million in EBITDA. As revenue scales toward the $600M run-rate, we expect EBITDA margins to converge with the industry standard (Cboe/Nasdaq) of 60-65%, implying that profitability will double even if revenue growth decelerates.

3. The „Optical“ Loss (GAAP vs. Cash Flow) Bearish investors are fixated on the headline GAAP Net Loss of ($102.1 million) in Q3 2025. This figure is mathematically distorted and irrelevant for forward valuation.

- Deconstructing the Loss: The loss was driven almost entirely by a $107.7 million one-time charge for the „extinguishment of debt.“ Following the August 2025 IPO (which raised ~$397M), MIAX aggressively paid off its expensive private credit facility (the 2029 Senior Secured Term Loan).

- The Reality: If you strip out this one-time accounting charge and the non-cash stock-based compensation (associated with IPO vesting), the company is operating cash flow positive.

- Balance Sheet Reset: Post-IPO, the company holds $401 million in cash against a trivial $6.5 million in debt. This is a fortress balance sheet that removes the „distress risk“ premium previously attached to the stock.

V. Valuation: The Private/Public Arbitrage

MIAX represents a classic „Category Error“ in valuation. The market is pricing it as a small-cap financial services firm, while smart money (like Horizon Kinetics) recognizes it as a nascent utility monopoly.

1. The „Horizon Kinetics“ Premium: The Asset Class Disconnect As noted in the Horizon Kinetics investment thesis, there is a massive valuation divide between private exchanges and public „Blue-Chip“ utilities.

- The „Moat“ Argument: Securities exchanges are the oldest continually operated companies in the world. They are natural monopolies protected by insurmountable regulatory barriers (it took MIAX 15 years to assemble its license portfolio).

- The MGEX Arbitrage: The acquisition of the Minneapolis Grain Exchange (MGEX) was the turning point. As HK noted, the clearing license (DCO) attached to MGEX is a „force multiplier“ for value. It allows MIAX to create its own products (like SPIKES) and keep 100% of the economics. The market is currently assigning zero value to the optionality of this license, pricing MIAX solely on its current options volume.

2. Relative Valuation (The Multiple Expansion Trade) At the current price of ~$41.75 (Market Cap ~$3.6B), MIAX is trading at a steep discount to its inferior peers.

| Metric | MIAX (The Challenger) | Cboe Global Markets (The Incumbent) | CME Group (The Utility) |

| P/S Ratio (NTM) | ~2.7x – 3.5x | ~5.5x | ~12.0x |

| Revenue Growth | +57% | +5% | +4% |

| EBITDA Margin | 44% (expanding) | 60% (mature) | 68% (mature) |

| Clearing Ownership | Yes (MGEX) | Yes | Yes |

The Thesis for Re-Rating:

- Phase 1 (Current): Stock trades at ~3x sales due to „IPO hangover“ and GAAP loss confusion.

- Phase 2 (2H 2026): As GAAP net income turns positive and margins hit 50%, the „distress discount“ vanishes. The stock re-rates to a conservative 6x Sales (parity with Cboe).

- Phase 3 (Long Term): As the proprietary futures business (Onyx) scales, the market begins to view MIAX as a „Mini-CME,“ commanding a 10x+ multiple.

3. Price Target Formulation

- Bull Case Revenue (2026E): $650M (assuming 25% growth & successful Sapphire ramp).

- Target Multiple: 6.5x Sales.

- Implied Market Cap: ~$4.2B.

- Implied Share Price: ~$60 – $65 (+50% Upside).

Conclusion: You are buying a „200-year asset“ (a fully licensed exchange and clearing house) at a startup valuation. The „optical“ losses from the IPO have created a temporary window to acquire this infrastructure monopoly at a fraction of its replacement cost. As Horizon Kinetics suggests, this is not just a trade; it is a permanent capital asset currently on sale.

VI. Comparative Fee Analysis (The „Subsidization War“)

To understand how MIAX steals market share, one must look at the „Maker-Taker“ economics. Below is a comparative analysis of the standard fee tiers for Penny Pilot Options (the most active contracts like SPY, AAPL, NVDA).

Note: Exchanges pay „Rebates“ (negative numbers) to attract orders and charge „Fees“ (positive numbers) to match them.

| Metric | MIAX Pearl (Aggressive Challenger) | Nasdaq PHLX (Legacy Incumbent) | Cboe BZX (Direct Competitor) | Commentary |

| Market Model | Maker-Taker | Pro-Rata / Hybrid | Maker-Taker | Pearl targets HFTs; PHLX targets Banks. |

| Maker Rebate (Max) | ($0.52) per contract | ($0.48) per contract | ($0.51) per contract | MIAX pays the highest rebate to liquidity providers, ensuring the tightest spreads. |

| Taker Fee (Max) | $0.50 per contract | $0.50 per contract | $0.50 per contract | Taker fees are capped by regulation, so MIAX competes on the rebate side. |

| Tier 1 Threshold | Low Volume Reqs | High Volume Reqs | Medium Volume Reqs | MIAX makes it easier for smaller firms to hit the highest rebate tiers (lower barrier to entry). |

| Routing Fees | Aggressive Caps | Standard | Standard | MIAX caps routing fees to keep flow „sticky“ within their 4-exchange ecosystem. |

Strategy: MIAX uses its lower corporate overhead to pass more economics back to the traders (Rebates). This effectively „bribes“ the algorithms to route orders to MIAX first. Once the volume is there, they can slowly raise fees (margin expansion).

VII. Key Risks: The Bear Case

While the growth thesis is compelling, MIAX operates in a highly regulated, leverage-sensitive environment. The following risks are non-trivial and require constant monitoring.

1. Regulatory Risk: The „Access Fee“ Squeeze (Reg NMS 2024/2025)

The single biggest threat to MIAX’s business model is not a competitor, but the SEC’s recent amendments to Regulation NMS.

- The Mechanism: In late 2024 (upheld by the D.C. Circuit in Oct 2025), the SEC reduced the „Access Fee Cap“ from 30 mils ($0.30 per 100 shares) to 10 mils ($0.10) for many securities.

- The Impact: MIAX Pearl’s entire „Maker-Taker“ strategy relies on charging a high Taker fee (e.g., $0.50 in options, though equities are tighter) to subsidize a massive Rebate (e.g., $0.52) to liquidity providers.

- The Squeeze: If regulators force similar cap reductions in the options market (a stated goal of the current SEC regime), MIAX’s ability to pay aggressive rebates evaporates. Without the rebate „bribe,“ the algorithmic glue holding liquidity on MIAX Pearl dissolves, and market share could revert to the incumbent „Pro-Rata“ exchanges (Cboe/Nasdaq) where institutional relationships matter more than price.

2. Market Structure Risk: Internalization & The „Wholesaler“ Threat

MIAX Sapphire was built specifically to capture retail flow from wholesalers like Citadel Securities and Virtu.

- The Risk: These wholesalers are not just clients; they are competitors. They have the ability to „internalize“ orders—executing them against their own inventory off-exchange—rather than routing them to a lit exchange like MIAX.

- PFOF Vulnerability: If the political wind shifts against „Payment for Order Flow“ (PFOF)—as seen with the recent EU ban fully effective in 2026—wholesalers may stop routing to „Taker-Maker“ venues entirely. If Citadel decides to internalize 80% of Robinhood’s flow instead of 60%, MIAX Sapphire’s volume could collapse overnight despite having superior technology.

3. Volume Sensitivity: The „VIX < 12“ Danger Zone

MIAX is a „high beta“ asset. Its revenue is inextricably linked to the velocity of trading (ADV).

- The Correlation: Exchange volumes are highly correlated with the VIX (Volatility Index).

- VIX > 20: Spreads widen, hedging activity explodes, and MIAX prints money (operating leverage).

- VIX < 12: In periods of extreme market complacency (e.g., 2017), option volumes atrophy. Because MIAX has a high fixed-cost base (technology/data centers), a 20% drop in industry volume can lead to a 40-50% drop in EBITDA.

4. Integration & Operational Risk: The „June 2025“ Warning

Investors should not ignore the operational hiccups that accompanied the recent expansion.

- The Sapphire Incident: On June 3, 2025, MIAX Sapphire experienced a critical „system difficulty“ where test data was accidentally injected into the live production environment, forcing a multi-hour trading halt.

- Reputation Damage: In the exchange world, uptime is the product. Broker-dealers have „kill switches“ that auto-disable an exchange if it glitches. If the integration of the MIAX Futures Onyx clearing platform experiences similar „teething issues,“ major Futures Commission Merchants (FCMs) like Goldman Sachs or JP Morgan will hesitate to route flow there, stalling the SPIKES growth story.

5. The „Control“ Discount (Voting Rights)

MIAX has a dual-class share structure (common in exchanges) that concentrates voting power in the hands of early management and strategic partners.

- Risk: Public shareholders have limited recourse if management decides to pursue „empire-building“ acquisitions (e.g., buying a crypto exchange) rather than returning capital to shareholders. This governance structure typically warrants a valuation discount relative to fully democratized peers.

VIII. Conclusion: The „Blue-Chip“ in Toddler’s Clothing

MIAX represents one of the most compelling structural disconnects in the current financial services landscape. It is a „Blue-Chip“ infrastructure asset disguised by the messy financials of a recent IPO. The market is currently pricing MIAX as a speculative, unprofitable tech „challenger“ (trading at ~3x sales), while the underlying reality is that of a vertically integrated, federally licensed utility with the unassailable moat of a 140-year-old clearing house.

1. The „Category Error“ Opportunity

The core of this trade is an arbitrage on market perception.

- The Market Sees: A newly public company with ugly GAAP losses, high leverage, and a „me-too“ exchange trying to fight Cboe and Nasdaq for scraps.

- The Reality: A cash-flow positive machine that has already won the war for relevancy (18% market share). The GAAP losses are a temporary accounting fiction caused by debt extinguishment and IPO vesting. When these one-time items roll off in 2H 2026, the P/E ratio will snap from „undefined“ to „attractive,“ forcing a violent re-rating by quantitative funds that screen for profitability.

2. The „Flywheel“ of Value

MIAX is no longer just a fast matching engine; it is a self-reinforcing ecosystem.

- The Technology (The Engine): Their proprietary „binary“ logic allows them to operate four exchanges for the cost of one. This operating leverage means that as they steal market share from Cboe, their margins expand faster than their revenue.

- The Clearing (The Moat): The MGEX acquisition is the „checkmate“ move. By owning the clearing house, MIAX has removed the „margin tax“ paid to third parties. Every contract traded on MIAX Futures Onyx is 100% margin accretive. This vertical integration is the only path to challenging the Cboe VIX monopoly—a feat no other challenger has attempted with a self-owned clearing stack.

- The Inventory (The Listings): Through TISE and BSX, MIAX has built a recurring revenue base of international listings that serves as a hedge against U.S. volatility.

3. The Asymmetry of the Trade

As Horizon Kinetics correctly identified, exchange operators are the „royalty collectors“ of global capitalism. They do not take balance sheet risk; they simply take a toll on every transaction.

- Downside Protection: Even in a bear case where growth stalls, the liquidation value of the exchange licenses (4x SEC Options Exchanges + 1x DCO Clearing License) provides a hard floor. As noted, the MGEX license alone is a scarce asset that cannot be easily replicated.

- Upside Optionality: You are paying for the core options business and getting the „Futures Alpha“ for free. If the SPIKES Volatility Index gains even 10% of the traction of VIX, or if the Onyx platform attracts meaningful crypto or agricultural flow, the stock could double or triple.

Final Thought: In 2009, buying ICE or CME was a „consensus“ trade. In 2026, buying MIAX is the „contrarian“ trade that offers the same structural economics at a fraction of the price. We are not betting on a new paradigm; we are betting that a 200-year-old business model (the exchange) will continue to work, and that the fastest, most cost-efficient operator will eventually be valued like a winner.