LandBridge Company LLC, a distinctive player in the Permian Basin’s Delaware Basin, reported its Q1 2025 earnings on May 7, 2025, delivering a compelling performance that underscores its unique position as a surface and water royalty company. Unlike traditional energy firms tethered to the volatility of oil and gas markets, LandBridge generates over 90% of its revenue from non-commodity-linked sources, primarily through surface operations and water management royalties. This capital-light, high-margin business model, coupled with strategic expansion and operational efficiency, drove remarkable financial results in the first quarter.

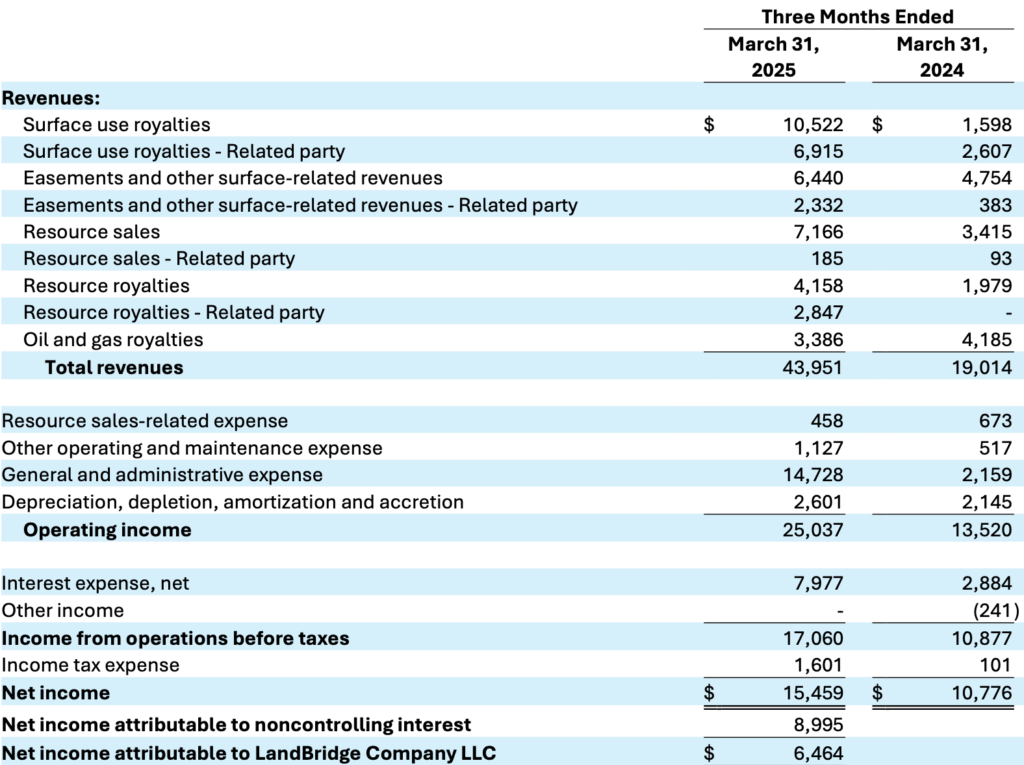

LandBridge achieved a standout quarter, with revenues reaching $44.0 million, a 131% increase from $19.0 million in Q1 2024 and a 20% rise from $36.7 million in Q4 2024. This performance exceeded consensus estimates of $43.12 million, reflecting robust demand for its services. The core driver of this growth lies in LandBridge’s revenue composition, where over 90% is derived from non-oil and gas sources. Surface royalties, stemming from fixed-fee agreements for rights-of-way, easements, and infrastructure usage, provide stable, predictable cash flows unaffected by commodity price swings. Water royalties, tied to the handling and recycling of produced water, capitalize on the Permian Basin’s high drilling and completion activity, further bolstering revenue. In Q1 2025, LandBridge managed 29.1 million barrels of produced water, a 36% year-over-year increase, highlighting its critical role in supporting operators’ sustainability efforts. Oil and gas royalties, while present, constitute less than 10% of revenue, minimizing exposure to the volatility of WTI crude or natural gas prices, which averaged $75-$80 per barrel and remained subdued, respectively, during the quarter.

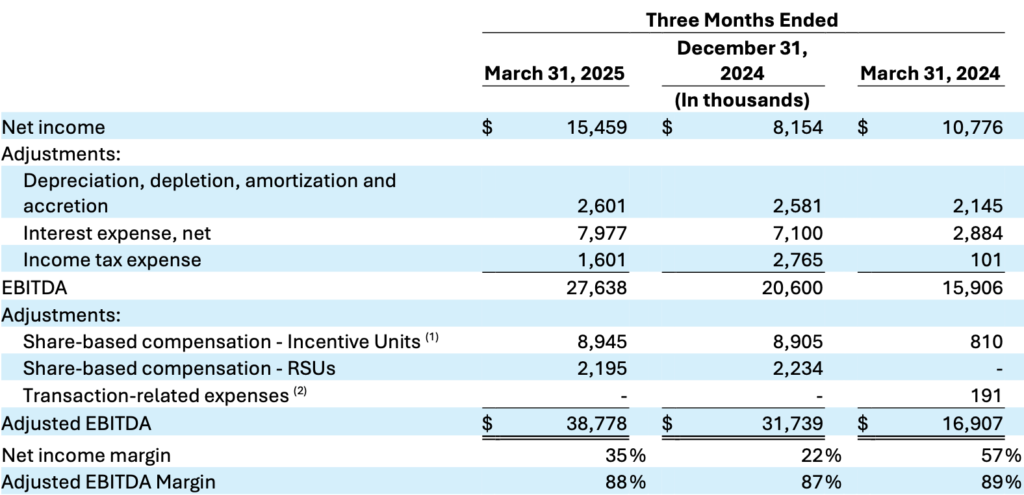

Profitability metrics further illustrate LandBridge’s efficiency. The company reported a net income of $15.5 million, translating to a 35% net income margin, a figure that stands out in an industry often constrained by operational costs. Adjusted EBITDA reached $38.8 million, up 129% year-over-year and 22% quarter-over-quarter, yielding an exceptional 88% EBITDA margin. This margin, among the highest in the sector, reflects the low-cost nature of LandBridge’s operations, where third-party operators bear the brunt of infrastructure and production expenses. Free cash flow generation was equally impressive at $15.8 million, with a 36% margin, providing ample liquidity to fund shareholder returns and growth initiatives.

LandBridge Company LLC’s balance sheet as of March 31, 2025, demonstrates a solid financial position, with $14.9 million in cash and cash equivalents and $379.3 million in total borrowings outstanding under its term loan and revolving credit facility. This results in a debt-to-EBITDA ratio of approximately 2.44x, calculated using annualized Q1 Adjusted EBITDA of $38.8 million, indicating moderate leverage while maintaining flexibility for growth initiatives. Capital expenditures were minimal at $0.1 million, reflecting LandBridge’s capital-light model, which prioritizes acquisitions of high-margin royalties generating land assets over infrastructure development. A significant strategic achievement in Q1 was the $17.8 million acquisition of approximately 5,200 net acres, contributing to LandBridge’s expanded holdings of approximately 277,000 surface acres across Texas and New Mexico, primarily in the Delaware Basin. This acquisition enhances LandBridge’s capacity to generate surface and water royalties, particularly through increased produced water volumes, positioning the company for sustained revenue and cash flow growth in a highly active region.

Operationally, LandBridge Company LLC distinguishes itself as a surface and water royalty company, leveraging its approximately 277,000 surface acres across Texas and New Mexico, primarily in the Delaware Basin, to generate high-margin royalties. These acres support diverse activities, including pipelines, roads, and produced water handling, which drive stable, activity-based revenue streams. In Q1 2025, LandBridge reported a significant increase in produced water royalty volumes, rising from 831 MBbls/d in Q4 2024 to 1,433 MBbls/d, a 72% sequential increase, fueled by strong organic growth and the Q4 2024 acquisition of 46,000 surface acres in the Wolf Bone Ranch. This surge reflects robust operator activity in the Permian Basin and underscores the growing demand for LandBridge’s water management services. The company’s operational efficiency is highlighted by its minimal capital expenditures of $0.1 million in Q1 2025, as third-party operators fund the infrastructure that generates LandBridge’s royalty income, reinforcing its capital-light model.

Strategically, LandBridge is well-positioned to capitalize on its strengths. Its capital allocation strategy balances growth and shareholder returns, with the $55 million acreage acquisition demonstrating a commitment to expanding its royalty base. Management noted a robust pipeline of future acquisition opportunities, supported by the company’s strong cash position. Looking ahead, LandBridge benefits from sustained operator activity in the Permian Basin, as evidenced by high rig counts and permits. Its over 90% non-oil and gas revenue insulates it from commodity price fluctuations, while its water management services align with regulatory and industry trends favoring sustainability.

However, risks remain. A slowdown in Permian Basin activity could reduce demand for surface and water services, though fixed-fee contracts mitigate this exposure. Acquisition execution, although a minor risk, is another consideration, as future deals must be accretive to sustain growth momentum. Regulatory changes in water management or environmental standards could pose challenges, though LandBridge’s ESG focus positions it to adapt. Compared to peers like Texas Pacific Land Corporation and Viper Energy Partners, LandBridge’s over 90% non-commodity revenue offers greater stability, while its 88% EBITDA margin matches or exceeds competitors. Its 131% revenue growth outpaces both, driven by a smaller base and strategic acquisitions.

In conclusion, LandBridge’s Q1 2025 earnings highlight its strength as a surface and water royalty company. The 131% year-over-year revenue growth and 88% EBITDA margin underscore its financial and operational prowess. We are confident in the ability of the LandBridge management to continue their recent success story and create long term shareholder value.