Executing the Playbook: Unpacking the „Surface Densification“ Engine, Free Cash Flow Surges, and the Alpha Digital Data Center Campus

When we reviewed LandBridge Company LLC’s (NYSE: LB) transformative fiscal 2025, we concluded that the company was proving to be a highly resilient, high-margin compounding machine built for the future of the Permian Basin. We noted that the company’s dual-engine strategy of optimizing surface-level energy infrastructure while actively cultivating its digital infrastructure optionality set it apart from passive legacy land banks.

LandBridge’s first-quarter 2026 results perfectly validate this thesis. Despite typical seasonal softness in the first quarter, LandBridge delivered massive year-over-year growth, an exceptional surge in free cash flow, and most following up on its data center „optionality“. Bolstered by increasing visibility into its commercial pipeline, management confidently raised full-year 2026 guidance.

Financial Performance: Cash Flow Conversion Takes Center Stage

LandBridge’s Q1 results showcase the sheer power of a capital-light model where the operator funds the infrastructure, and the landowner collects the toll.

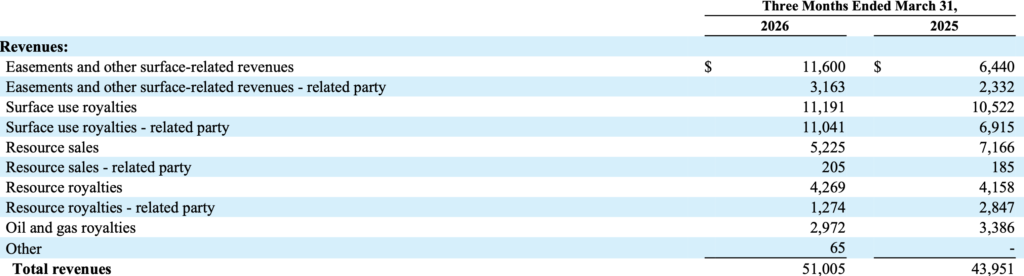

- Revenue: Total revenues for the first quarter came in at $51.0 million. While this represents an anticipated 11% sequential dip from Q4 2025, which management attributed to the natural seasonality of E&P capital cycles and the lumpiness of commercial agreements, it marks a robust 16% year-over-year increase.

- Adjusted EBITDA: The company delivered Q1 Adjusted EBITDA of $44.9 million, matching the 16% year-over-year top-line growth. Crucially, the Adjusted EBITDA margin remained elite at 88%, mirroring the structural profitability we highlighted throughout 2025.

- Free Cash Flow: Here is where the compounding nature of the business truly shines. LandBridge generated $40.9 million in Free Cash Flow for the quarter. This is a staggering 158% increase year-over-year with an 80% FCF margin. As management noted, $0.80 of every revenue dollar converts directly to free cash flow on minimal capital investment.

Under the Hood: The „Surface Densification“ Engine

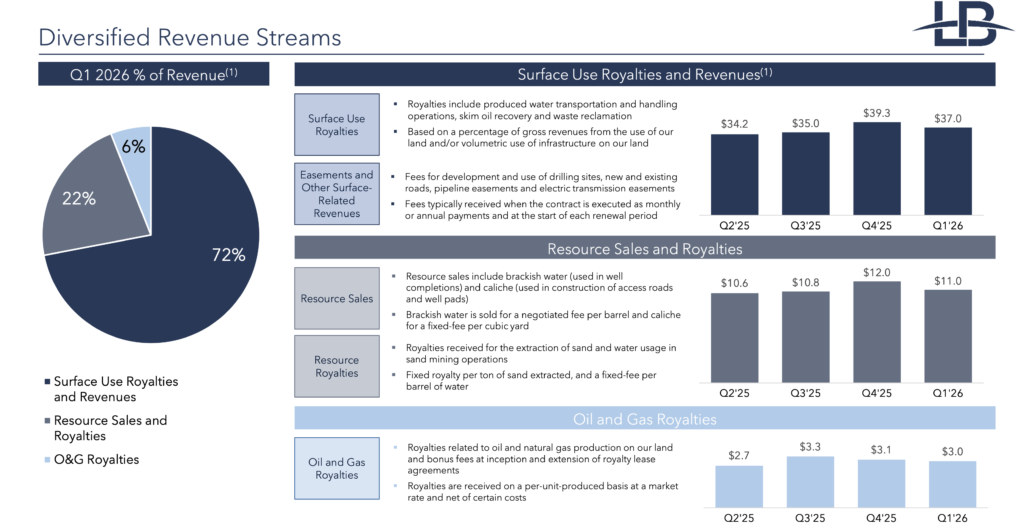

Unlike traditional E&P companies, or even legacy mineral royalty companies that rely heavily on the physical extraction of hydrocarbons, LandBridge is actively engineered to be an infrastructure toll-collector. The Q1 revenue mix highlights a deliberate decoupling from short-term commodity price volatility: roughly 72% from surface use, 22% from resources, and just 6% from direct oil and gas royalties.

1. Surface Use Royalties (The Core Engine): This segment generated $37.0 million in the quarter, representing a massive 41% year-over-year increase. This growth is driven by the company’s focus on actively „densifying“ or „stacking“ commercial activity on their acreage.

Management emphasized the critical distinction between LandBridge and its competitors: fee surface ownership. By owning the surface outright, rather than relying on BLM or state leaseholds that require periodic renewal, LandBridge provides developers with permanent control and multi-decade certainty. This permanence acts as a structural moat.

Furthermore, LandBridge’s symbiotic relationship with WaterBridge remains a massive catalyst. WaterBridge currently operates approximately 1.5 million barrels a day of infrastructure on LandBridge property. With „Project Speedway Phase 1“ coming online this summer and ramping through 2028, LandBridge is positioned to capture compounding royalty streams without deploying a single dollar of capital.

2. Resource Sales and Royalties: Representing about 22% of revenue ($11.0 million in Q1), this is the segment most immediately impacted by upstream development activity. LandBridge monetizes the physical materials necessary for basin development, specifically the sale of sand and the provision of supply water, operating at exceptionally high margins.

3. Active Acreage Expansion: Rather than passively managing a static land bank, LandBridge is constantly feeding its compounding engine. The company has added nearly 50,000 surface acres over the past year (including 5,700 acres in Q1) at highly disciplined valuations of roughly $1,000 per acre. By maintaining strict underwriting criteria, focusing onlyon fee surface ownership, every acquired acre immediately strengthens their long-term platform.

The Digital Infrastructure Catalyst: The Alpha Digital Campus

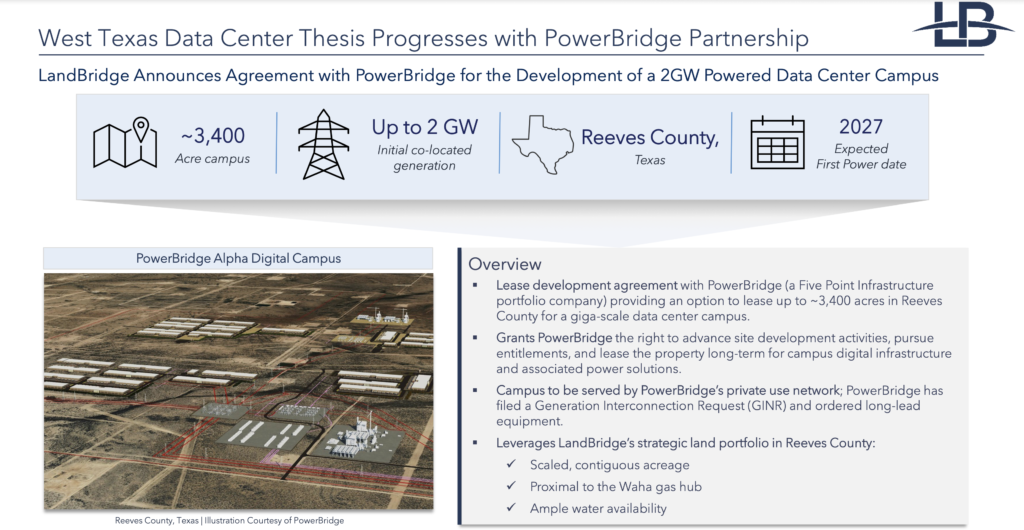

Perhaps the most significant strategic development in Q1 was the crystallization of LandBridge’s digital infrastructure strategy. In 2025, the narrative centered around high-level positioning. In Q1 2026, that narrative converted into direct economics.

LandBridge announced a landmark agreement with PowerBridge for the lease and development of the Alpha Digital data center campus in Reeves County, Texas.

- The Deal: PowerBridge secured a one-year option to lease up to 3,400 acres for a gigascale campus, resulting in an immediate $2.6 million option payment recognized in Q1.

- The Scale: The site is targeting up to 2 gigawatts of initial power generation capacity, with initial power delivery expected late next year and large-scale generation online in 2028.

This deal validates the core thesis: West Texas is rapidly becoming the next major U.S. data center hub. The region offers low-cost power, abundant water, fiber connectivity, and crucially, a favorable regulatory environment. LandBridge specifically benefits from its heavy footprint on the Texas side of the Texas/New Mexico border, providing the consistent permitting environment that hyperscalers demand. Because LandBridge owns the surface in fee, they can offer the multi-decade campus commitments that data center developers require, securing a long-duration lease with royalty economics that scale as the campus grows.

Capital Allocation and Upgraded Outlook

LandBridge’s pristine balance sheet allowed for robust shareholder returns in Q1. The company utilized its surging free cash flow to:

- Pay down $25.2 million of debt, lowering its net leverage ratio to 2.7x (targeting a long-term ratio of 2.0x to 2.5x).

- Maintain total liquidity of nearly $260 million.

- Declare a quarterly cash dividend of $0.12 per share, while maintaining its opportunistic $50 million share repurchase program.

Signaling deep conviction in the operational machinery and the quarters ahead, management raised its full-year 2026 Adjusted EBITDA outlook to $210 million to $230 million. Management cited increased visibility into committed commercial surface activity for Q2 through Q4, the looming ramp-up of WaterBridge’s Speedway project, and a highly supportive macro backdrop.

Conclusion

LandBridge’s first quarter of 2026 acts as a seamless extension of its record-breaking 2025. The company’s active land management approach continues to extract more value out of every surface acre, driving a 158% surge in free cash flow and sustaining elite 88% EBITDA margins. Meanwhile, the Alpha Digital data center agreement proves that LandBridge’s next-generation infrastructure ambitions are highly monetizable right now. LandBridge remains one of the most structurally advantaged land companies in the public markets, perfectly positioned to scale the Permian’s next great era of industrial development.