Asset-Light Compounding at the Heart of the Delaware Basin

When we reviewed LandBridge Company LLC’s (NYSE: LB) third-quarter results, we highlighted the sheer operating leverage inherent in its surface ownership model. The company’s fourth-quarter and full-year 2025 results, released this week, emphatically reinforced that thesis. Closing out a transformative fiscal year, LandBridge delivered exceptional top-line growth, unparalleled profit margins, and initiated a robust suite of shareholder return programs.

Much like the legacy land companies that preceded it in the region, LandBridge is proving that perpetual surface rights in the core of the Permian Basin—specifically the highly active Delaware sub-basin—offer one of the most distinctive, capital-light business models in the modern public markets. Yet, LandBridge differentiates itself with a highly active management approach and a forward-looking strategy that embraces both traditional hydrocarbons and the looming digital infrastructure boom.

The quarter reaffirmed LandBridge’s identity not merely as a passive land bank, but as a structural royalty compounder whose intrinsic value grows sequentially in step with the ongoing industrialisation of West Texas and New Mexico.

Financial Performance: The Power of 90% Margins

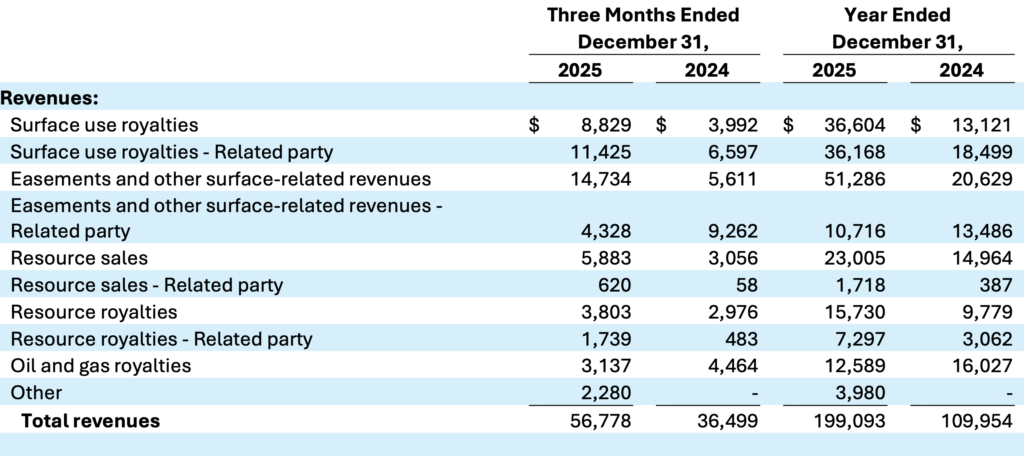

LandBridge’s fourth-quarter results are a testament to the structural advantages of a royalty and surface-fee model. The company reported total revenues of US $56.8 million for Q4 2025, representing a 12 percent sequential increase from Q3 and a massive 56 percent jump year-over-year. For the full year 2025, revenues reached US $199.1 million, an 81 percent surge compared to 2024.

What stands out most, however, is the profitability of these revenues.

- Adjusted EBITDA: The company delivered Q4 Adjusted EBITDA of US $51.1 million, up 61 percent year-over-year and 14 percent sequentially. This translates to an astonishing 90 percent Adjusted EBITDA margin for the quarter. Full-year Adjusted EBITDA stood at US $177.2 million, an 83 percent year-over-year increase, matching an 89 percent margin.

- Free Cash Flow: Because the company incurs virtually no capital expenditures to generate this fee-based income, the cash conversion is extraordinary. Q4 Free Cash Flow was US $36.4 million (a 64 percent margin), and full-year Free Cash Flow reached an impressive US $122.0 million (a 61 percent margin).

- Net Income Nuance: GAAP Net Income for the quarter came in at US $18.2 million (a 32 percent margin). Astute investors should note that this figure was heavily burdened by non-cash accounting items, including US $9.4 million in non-cash charges related to LandBridge Holdings LLC incentive units, US $2.3 million in restricted share unit charges, and US $5.8 million of transaction-related expenses. Excluding these items, the underlying cash-generating power of the business remains pristine.

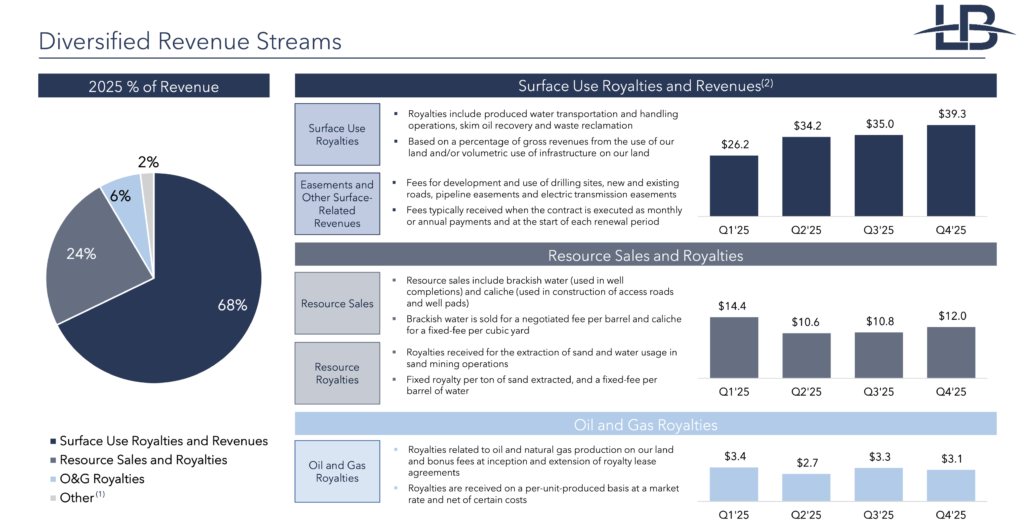

Segment Analysis: Surface Use and the Water Ecosystem

The engine of LandBridge’s growth remains its surface use and resource sales segments, which vastly outpace its direct oil and gas royalties. In fact, traditional oil and gas royalties contributed just a fraction of total revenue, decreasing slightly by US $0.2 million sequentially in Q4. This intentional weighting makes LandBridge a vital infrastructure toll-collector rather than a commodity producer.

Surface Use Royalties and Revenue: This segment is the crown jewel, generating US $39.3 million in the fourth quarter. This represents a US $4.3 million (or 12 percent) sequential increase from Q3. The growth was driven by continued structural increases in produced water handling royalties and a flurry of new easement payments.

In 2025 alone, the company executed approximately 450 new easements and agreements across its acreage. Every time an operator needs to lay a gathering pipe, build a lease road, or install a power transmission line, LandBridge collects a fee.

Resources Sales and Royalties: Adding US $12.0 million to the top line in Q4, this segment grew by US $1.3 million (or 12 percent) sequentially. LandBridge monetizes the physical materials required for basin development, seeing elevated revenues from supply water royalty volumes and sand sales during the quarter.

Surface Use Economic Efficiency (SUEE): A critical metric for tracking LandBridge’s operational success is how well management „densifies“ the commercial activity on its land. The company delivered massive improvements in its per-acre revenue yields throughout 2025, validating management’s active approach:

- Legacy Acreage: SUEE increased to US $1,159 per acre in 2025, representing a 14 percent increase from US $1,018/acre in 2024 and an incredible 149 percent increase from just US $465/acre in 2022.

- Acquired Acreage: Acreage acquired during 2024 (including massive additions in the Wolf Bone Ranch and Winkler/Lea counties) saw a 145 percent SUEE increase, jumping from US $204/acre in 2024 to US $499/acre in 2025.

Management is not just passively holding land; they are systematically stacking multiple cash-flow streams (water, sand, roads, pipelines) on top of the same acreage footprint.

The Digital Infrastructure Catalyst

As we noted in our previous reviews, surface acreage in the Permian is no longer just about oil, gas, and water. It is rapidly becoming ground zero for the next wave of industrial development: renewable energy and data centres.

LandBridge is actively cultivating this optionality. While the company’s foundation rests on supporting traditional energy, its vast, contiguous acreage and access to critical power infrastructure make it an ideal host for power-hungry digital infrastructure.

In December 2025, LandBridge announced development agreements with subsidiaries of Samsung C&T Renewables, LLC. These agreements provide the option to lease acreage for two potential Battery Energy Storage System (BESS) projects in Pecos and Loving counties, Texas, with an aggregate capacity of 350 MW. By positioning itself as an enabler for both traditional energy extraction and next-generation grid stability and compute infrastructure, LandBridge is creating a revenue stream that is completely decoupled from the hydrocarbon cycle.

Capital Allocation and Balance Sheet Optimization

LandBridge’s financial posture was significantly fortified as it closed out the year, transitioning from a growth-at-all-costs setup to a balanced, institutional-grade compounding structure.

In November 2025, the company executed a major refinancing, closing an inaugural US $500.0 million offering of 6.25% senior unsecured notes due 2030 and establishing a new US $275.0 million senior secured revolving credit facility. LandBridge ended the year with total borrowings of US $570.0 million and US $30.7 million in cash and cash equivalents.

Given the company’s immense cash generation and near-90 percent EBITDA margins, this leverage profile is highly manageable. Crucially, the refinancing improved LandBridge’s cost of capital and provided approximately US $205.0 million in available borrowing capacity under the new revolver to fund opportunistic acreage acquisitions.

With the balance sheet optimized, management has aggressively shifted toward returning capital to shareholders:

- Dividend Hike: The Board declared a quarterly cash dividend of US $0.12 per Class A share for the first quarter of 2026—a 20 percent increase from prior levels.

- Share Repurchases: Signaling deep confidence in the company’s intrinsic value and structural growth trajectory, LandBridge announced that its Board of Directors authorized a new US $50 million share repurchase program.

Long-Term Outlook: 2026 and Beyond

Looking ahead, management provided a highly constructive outlook for the coming year, forecasting full-year 2026 Adjusted EBITDA between US $205 million and US $225 million. At the midpoint, this represents greater than 20 percent projected year-over-year growth.

The thesis for LandBridge remains clean and compelling: own mission-critical surface real estate in the most active energy basin in the United States, aggressively manage the land to drive up per-acre yields (SUEE), and return the resulting free cash flow to shareholders.

While legacy peers in the basin have spent a century passively compounding, LandBridge is executing a modern, accelerated version of this playbook. Between its traditional pipeline and water easements, its synergistic relationship with WaterBridge, and its growing pipeline of solar, battery storage, and data centre projects, LandBridge is proving to be a highly resilient, high-margin compounding machine built for the future of the Permian Basin.