Texas Pacific Land Corporation (TPL), one of the largest landowners in Texas with approximately 873,000 acres concentrated in the Permian Basin, reported its Q1 2025 earnings on May 7, 2025, delivering a robust performance driven by its unique position as a surface and royalty company. TPL generates revenue through surface-related activities and royalties, with a significant emphasis on water management and oil and gas royalties. This capital-light, high-margin business model, coupled with strategic acquisitions and operational efficiency, resulted in great financial metrics for the first quarter.

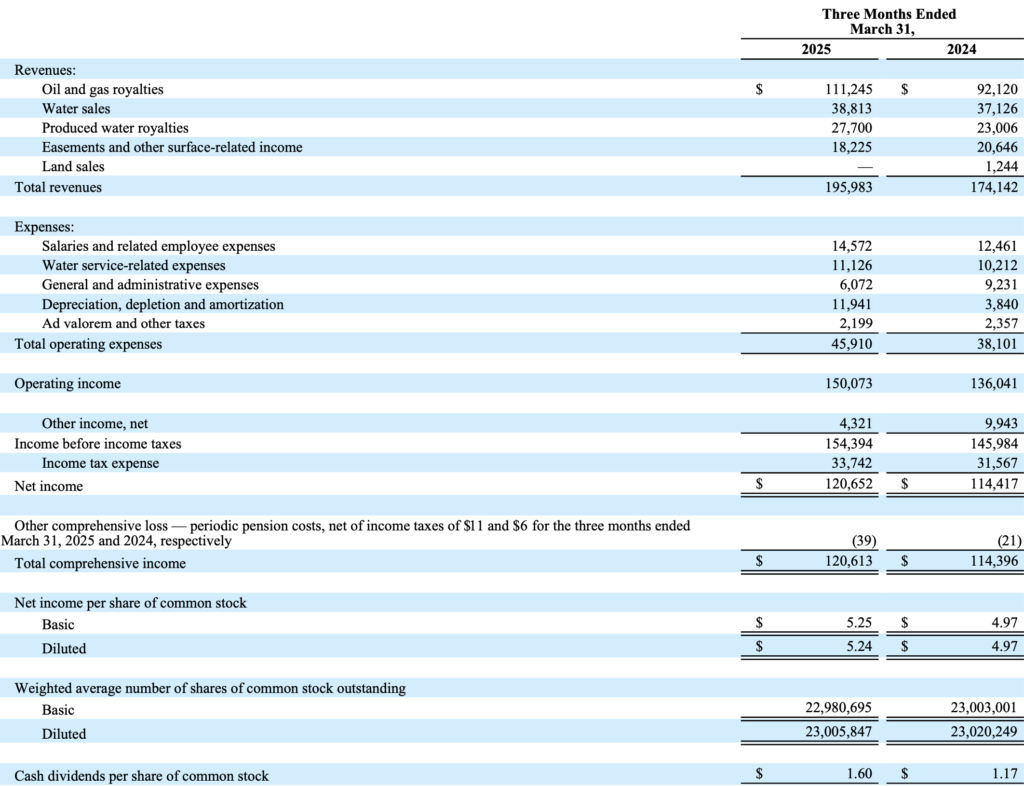

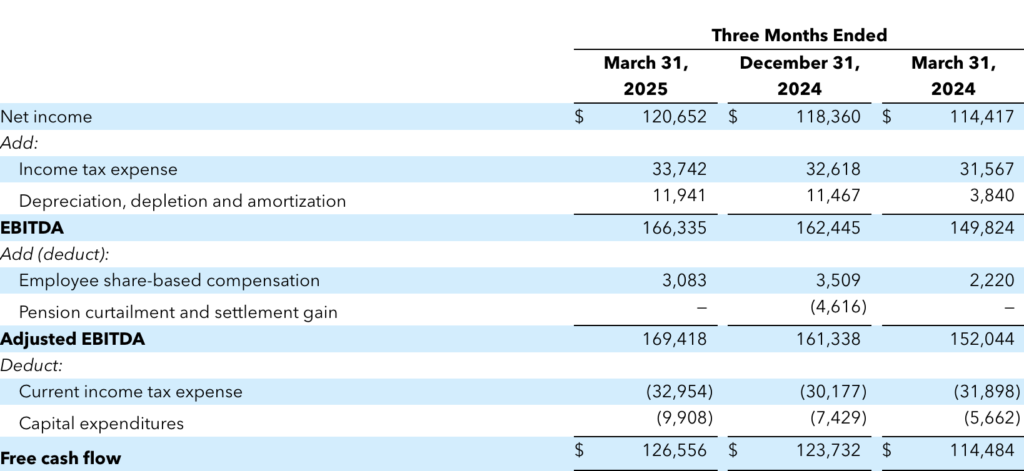

Financially, TPL achieved exceptional results in Q1 2025, with total revenues reaching $196.0 million, an 11% increase from $174.1 million in Q1 2024 and a 5% sequential increase from $185.8 million in Q4 2024. This growth was propelled by a $14.3 million rise in oil and gas royalty revenue, reflecting record royalty production of 31.1 thousand barrels of oil equivalent (Boe) per day, and a $2.1 million increase in water sales, contributing to record Water Services and Operations segment revenues of $69.4 million. Net income for the quarter was $120.7 million, or $5.24 per diluted share, up 5% from $114.4 million ($4.97 per share) in Q1 2024, yielding a net income margin of approximately 62%. Adjusted EBITDA reached $169.4 million, with an impressive 86% margin, underscoring the company’s ability to convert revenue into high-margin cash flows. Free cash flow (FCF) was a standout at $126.6 million, reflecting an FCF margin of 65%, which supports TPL’s shareholder-friendly capital allocation strategy. The company declared a quarterly cash dividend of $1.60 per share, payable on June 16, 2025, to shareholders of record as of June 2, 2025, affirming its commitment to returning capital to investors.

The composition of TPL’s revenue highlights its diversified, high-margin model. Oil and gas royalties, which are still accounting for a significant portion of revenue, benefited from the record 31.1 thousand Boe per day production, driven by strong operator activity in the Permian Basin. The Water Services and Operations segment, generating $69.4 million, was bolstered by increased water sales and produced water royalties, reflecting TPL’s critical role in supporting Permian operators’ water management needs. Surface-related revenues, including easements, leases, and material sales (caliche), provided stable, non-commodity-linked cash flows, mitigating exposure to oil and gas price volatility. Notably, over 50% of TPL’s revenue is derived from non-oil and gas sources, such as water and surface activities, which enhances financial stability. The 86% Adjusted EBITDA margin and 65% FCF margin are exceptional, driven by TPL’s capital-light model, where third-party operators fund infrastructure development, leaving TPL to collect royalties with minimal operational costs.

TPL’s balance sheet remains a fortress, with no debt and ample cash reserves. The company’s debt-free status and robust liquidity, highlighted by CEO Tyler Glover’s commentary on navigating potential industry downturns, provide significant financial flexibility. Capital expenditures remain low. The absence of debt and strong FCF generation position TPL to capitalize on market opportunities, such as consolidating fragmented royalty and surface assets in the Permian Basin.

Operationally, TPL’s approximately 873,000 surface acres support a wide range of activities, including pipelines, roads, water sourcing, produced water treatment, and saltwater disposal, all generating fixed or activity-based royalties. The Water Services and Operations segment achieved record performance, with $69.4 million in revenue, driven by increased water sales and a surge in produced water royalties. TPL’s strategic investments in water infrastructure, including a sub-scale produced water desalination test facility under construction (targeted for mid-2025 completion). The company’s royalty acreage supported 31.1 thousand Boe per day in production.

Strategically, TPL is still well-positioned for growth. The company’s focus on next-gen opportunities, such as water desalination and potential digital infrastructure leases, complements its core royalty business. The earnings release highlights ongoing commercial discussions for non-hydrocarbon projects, signaling diversification beyond traditional energy. TPL’s acquisition strategy remains active, with prior deals in 2024 (e.g., 7,490 net royalty acres for $275.2 million in Q4) demonstrating its ability to deploy capital accretively. CEO Tyler Glover emphasized TPL’s resilient business model, noting its ability to generate high-margin cash flows regardless of commodity price fluctuations, a critical advantage in an uncertain economic environment.

Risks include potential slowdowns in Permian Basin activity, which could reduce royalty and water revenues, though TPL’s >50% non-commodity revenue provides a buffer. Commodity price volatility, with WTI crude averaging $75-$80 per barrel in Q1 2025, poses a risk to oil and gas royalties, but TPL’s diversified streams mitigate this exposure. Acquisition execution is another consideration, as future deals must remain accretive. Compared to peers like LandBridge Company LLC, TPL’s 86% EBITDA margin is comparable (LandBridge: 88%), but its debt-free status and larger 873,000-acre footprint provide a competitive edge.

In conclusion, TPL’s Q1 2025 earnings underscore its strength as a surface and royalty company, with $196.0 million in revenue, $120.7 million in net income, and $126.6 million in FCF driving a high-margin, capital-light model. Record 31.1 thousand Boe per day production and $69.4 million in water revenue highlight its Permian Basin leadership. Although we would like to see increase in land acquisitions, Texas Pacific Land Corp. remains our favorite compounder. Their almost 1.000.000 acres are a one of a kind asset that is managed by one of the greatest teams with a keen focus on generating long term shareholder value.